Learn smarter with fresh insights from our tutors.

Practical study guides, course supplements, and learning resources curated to help you move faster through every subject.

Strengthening Data Privacy Laws in an Era of Digital Transformation

Strengthening Data Privacy Laws in an Era of Digital Transformation

Welcome to the digital age, where information flows freely and our lives are intricately intertwined with technology. From social media to online shopping, we now rely on vast amounts of data being shared and stored across various platforms. But with great convenience comes great responsibility - the need for robust data privacy laws has become more pressing than ever before.

In this blog post, we will dive into the world of data privacy and explore why stronger regulations are essential in today's era of digital transformation. We'll uncover the challenges faced in enforcing these laws, examine their impact on businesses, and propose potential solutions to strengthen them. So buckle up as we embark on a journey through the complexities of protecting our personal information in an increasingly interconnected world!

The Need for Stronger Data Privacy Laws

In today's digital age, where personal and sensitive information is constantly being shared and stored online, there is a pressing need for stronger data privacy laws. These laws are crucial in protecting individuals from the potential misuse or unauthorized access to their data.

One of the main reasons why stronger data privacy laws are necessary is the increasing number of cyber threats and data breaches. Hackers are becoming more sophisticated in their methods, making it easier for them to gain access to personal information. Without robust regulations in place, individuals have little protection against these attacks.

Furthermore, as technology continues to advance at a rapid pace, so does the amount of data that companies collect on their customers. This vast trove of information can be valuable for businesses but also poses significant risks if not handled properly. Stronger data privacy laws would help ensure that companies implement proper security measures and obtain informed consent before collecting or sharing any personal information.

Another key factor driving the need for stronger data privacy laws is the rise of social media platforms and other online services that extensively collect user data for targeted advertising purposes. While these services may offer convenience and personalized experiences, they often come at the expense of individual privacy. With stricter regulations in place, users would have more control over how their personal information is used by these platforms.

Moreover, with globalization blurring geographical boundaries when it comes to handling personal data, harmonized international standards become essential. The worldwide nature of digital transactions calls for unified efforts in establishing robust frameworks that protect user rights globally.

Strong data privacy laws are vital in this era of digital transformation to safeguard individuals' sensitive information from being exploited or misused by hackers or businesses alike. These regulations should aim to strike a balance between empowering consumers with control over their own data while ensuring smooth business operations across various industries.

The Challenges of Enforcing Data Privacy Laws

Enforcing data privacy laws in the era of digital transformation presents a myriad of challenges. One major obstacle is the rapid advancement of technology itself, which often outpaces legislation and enforcement efforts. With new technologies emerging constantly, it can be difficult for lawmakers to keep up with the evolving landscape of data collection and usage.

Additionally, there are issues surrounding jurisdictional boundaries in enforcing data privacy laws. The internet knows no borders, making it challenging to regulate the flow of information across different countries and legal systems. This lack of uniformity can lead to gaps in protection for individuals' personal information.

Another challenge lies in distinguishing between legitimate data practices and those that infringe upon privacy rights. It requires expertise from both legal professionals and technical experts to determine whether companies are handling personal data responsibly or engaging in potentially harmful practices such as unauthorized sharing or selling.

Furthermore, enforcement agencies face resource constraints when trying to monitor compliance with these laws effectively. As technology becomes increasingly complex, so do investigations into potential violations. Limited budgets and personnel make it difficult for authorities to stay ahead of sophisticated cybercriminals who may exploit weaknesses in security measures.

Overcoming these challenges requires collaboration between governments, regulatory bodies, businesses, and individuals themselves. Efforts should focus on harmonizing global standards for data protection while also investing in education and training programs that raise awareness about individual rights regarding their personal information.

In summary, enforcing robust data privacy laws remains an ongoing battle amidst escalating digitalization efforts worldwide. While significant progress has been made over the years, challenges persist due to technological advancements outpacing legislation's ability to catch up adequately. Addressing these obstacles will require concerted efforts from all stakeholders involved – governments implementing comprehensive regulations; businesses prioritizing ethical handling of customer data; individuals actively advocating for their own privacy rights; and international cooperation towards establishing consistent guidelines across jurisdictions.

The Impact of Data Privacy Laws on Businesses

Data privacy laws have had a significant impact on businesses around the world. With the increasing digitization of information and the growing concern over data breaches, it is essential for companies to prioritize data protection.

One key impact of data privacy laws is that businesses are now held accountable for how they collect, store, and use customer data. This means that companies must implement robust security measures to safeguard sensitive information and ensure compliance with legal requirements.

Moreover, these laws also give individuals more control over their personal data. Customers now have the right to know what information businesses hold about them and can request its deletion or correction if necessary. This has forced organizations to be transparent about their data practices and establish processes for handling such requests.

In addition, the implementation of stringent data privacy regulations has led to increased consumer trust in businesses. When customers feel confident that their personal information is being protected, they are more likely to engage with brands and share valuable insights. As a result, companies can build stronger relationships with their target audience and gain a competitive edge in the market.

However, it's important to acknowledge that complying with data privacy laws can also pose challenges for businesses. The costs associated with implementing new security measures and ensuring compliance can be significant, particularly for smaller enterprises with limited resources.

Furthermore, as technology continues to advance at a rapid pace, keeping up with evolving regulations becomes increasingly complex. Companies may require ongoing training programs or even dedicated staff members responsible for staying up-to-date on changes in legislation surrounding data privacy.

While there might be some challenges involved in adhering to strict data privacy laws, the benefits outweigh them significantly. By prioritizing customer trust through robust security practices and transparent policies regarding personal information handling - businesses not only protect their reputation but also foster strong relationships built on trust

Proposed Solutions to Strengthen Data Privacy Laws

1. Enhanced Regulation and Oversight: One proposed solution is the implementation of stronger regulations and oversight mechanisms to ensure compliance with data privacy laws. This can include stricter penalties for non-compliance, regular audits of organizations handling personal data, and increased transparency in data practices.

2. Education and Awareness Campaigns: Another solution involves raising awareness about the importance of data privacy among individuals and businesses. Educating people on their rights regarding their personal information can help empower them to make informed decisions about how their data is used and shared.

3. International Collaboration: Given that digital transformation transcends borders, it is crucial for countries to work together in establishing global standards for data protection. International collaboration can facilitate the exchange of best practices, harmonize regulations across jurisdictions, and promote a more consistent approach towards protecting personal information.

4. Technological Innovations: Advancements in technology can play a significant role in strengthening data privacy laws. For instance, implementing robust encryption techniques or developing secure identity verification systems can enhance the security of sensitive information against unauthorized access or breaches.

5. Ethical Considerations: Integrating ethical principles into data collection and usage practices is essential for safeguarding individual privacy rights. Adhering to ethical guidelines such as obtaining explicit consent, minimizing unnecessary data collection, and using anonymization techniques where appropriate helps protect individuals' privacy while still enabling innovation.

6. Collaboration between Businesses & Governments - Establishing partnerships between businesses and governments fosters an environment where both entities work together towards ensuring strong data protection measures are implemented effectively at scale.

7. Investment in Research & Development - Allocating resources towards research on emerging technologies like artificial intelligence (AI) that have implications on user privacy will enable policymakers to anticipate potential challenges proactively rather than reactively responding after harm has occurred.

By adopting these proposed solutions collectively or individually depending on specific contexts, we can strengthen our existing framework around data privacy laws and better protect individuals' personal information in this era of digital transformation.

Conclusion

In an era of digital transformation, where data is the new currency, strengthening data privacy laws has become a paramount task. The need for stronger regulations to protect individuals' personal information and maintain their trust in the digital world cannot be emphasized enough.

While there are challenges in enforcing these laws, such as jurisdiction issues and technological advancements outpacing legislation, it is crucial that governments and regulatory bodies take proactive measures to address these hurdles. Collaboration between countries and international organizations can also play a significant role in harmonizing data protection standards globally.

Businesses must recognize that compliance with robust data privacy laws is not just an obligation but also an opportunity to enhance customer loyalty and build a strong brand reputation. By prioritizing privacy as a fundamental aspect of their operations, organizations can foster transparency, accountability, and ultimately gain customers' confidence.

To strengthen data privacy laws effectively, proposed solutions include comprehensive legislation that covers all aspects of data processing along with clear guidelines on consent management and breach notifications. Regular audits by independent authorities can ensure adherence to these regulations while imposing strict penalties for non-compliance acts as a deterrent.

Moreover, investing in technology solutions like encryption techniques and anonymization tools will further safeguard sensitive information from unauthorized access or misuse. Additionally, educating individuals about their rights regarding their personal data empowers them to make informed decisions about sharing their information online.

In conclusion (without explicitly stating so), as our lives become increasingly intertwined with technology, securing our personal information should be everyone's concern – governments need to enact stringent legislation; businesses must prioritize data protection; individuals ought to stay vigilant about how their information is being used. Only through collective action can we create a more secure digital landscape where privacy remains intact amidst the rapid pace of innovation.

Understanding Regulatory Capture: Its Causes and Consequences

Understanding Regulatory Capture: Its Causes and Consequences

Regulatory capture: a term that might sound complex and intimidating, but it's something we should all be aware of. Just imagine a scenario where the very institutions meant to regulate certain industries end up being controlled or influenced by those very industries themselves. Sounds alarming, right? Well, this is exactly what regulatory capture is all about.

In today's blog post, we will dive deep into the world of regulatory capture – what it means, its causes, consequences, and most importantly, how we can prevent it. So buckle up and get ready for an eye-opening exploration into this critical issue that affects us all. Let's begin!

What is Regulatory Capture?

Regulatory capture refers to a situation where regulatory agencies, which are supposed to act in the public's interest and ensure fair competition, end up being influenced or controlled by the industries they are meant to regulate. Instead of serving as independent watchdogs, these agencies may develop cozy relationships with industry players, leading to biased decision-making that favors their interests over those of the general public.

This phenomenon occurs when regulatory bodies become captives of the very industries they were established to oversee. It can manifest in various ways: through direct lobbying and campaign contributions from industry representatives, revolving door appointments where regulators move into lucrative positions within the industries they once regulated, or even subtle forms of influence such as providing expert advice or shaping legislation in favor of specific companies or sectors.

The consequences of regulatory capture can be far-reaching and detrimental for society. When regulations are crafted or enforced based on industry preferences rather than public welfare considerations, it leads to market distortions, reduced competition, higher prices for consumers, lower quality products and services, and limited innovation. Moreover, this imbalance undermines trust in government institutions and erodes democratic principles.

Preventing regulatory capture is crucial for maintaining fairness and ensuring effective regulation. Transparency is key – clear guidelines should be established regarding interactions between regulators and industry stakeholders. Strong ethical standards must be upheld by both regulators themselves as well as the industries under scrutiny. Additionally, fostering a diverse pool of talent within regulatory agencies can help mitigate biases while enhancing expertise.

In conclusion (oops!), understanding what regulatory capture is empowers us all to recognize its signs and take action against it. By promoting transparency and accountability within our regulatory frameworks, we pave the way towards a more equitable society where regulations truly serve the best interests of everyone involved.

Causes of Regulatory Capture

1. Industry Influence: One major cause of regulatory capture is the close relationship between regulators and the industries they oversee. Regulators may become too cozy with industry leaders, leading to a conflict of interest that undermines their ability to effectively regulate.

2. Revolving Door Phenomenon: The revolving door between government agencies and private sector organizations can also contribute to regulatory capture. When regulators leave their positions to work for the same industries they once regulated, it creates a perception of bias and raises concerns about undue influence.

3. Information Asymmetry: Another factor contributing to regulatory capture is information asymmetry. Industries often possess more knowledge about their operations than regulators do, making it easier for them to manipulate the system in their favor.

4. Lack of Resources: Insufficient funding or staffing levels within regulatory agencies can make them vulnerable to capture by well-resourced industries. When regulators are stretched thin, they may be more susceptible to industry pressure or influence.

5. Political Interference: Political interference in regulatory processes can also lead to capture. Politicians may prioritize short-term political gain over long-term public interest, influencing decisions made by regulators.

It's crucial for policymakers and stakeholders alike to recognize these causes and take steps towards preventing regulatory capture in order to ensure fair and effective regulation that serves the best interests of society as a whole.

Consequences of Regulatory Capture

1. Erosion of Public Trust: When regulatory capture occurs, it undermines the public's confidence in the regulatory system and the government's ability to protect their interests. This erosion of trust can lead to a loss of faith in institutions and a growing cynicism towards regulations.

2. Distorted Policies: Regulatory capture often results in policies that are skewed towards benefiting the captured industry or interest group, rather than serving the broader public interest. This can lead to unfair advantages for certain companies or sectors, while stifling competition and innovation.

3. Ineffective Regulation: As regulators become influenced by those they are supposed to regulate, enforcement may become lax or inconsistent. The captured regulators may turn a blind eye to violations within the industry or adopt lenient penalties, thereby failing to effectively address issues such as consumer protection or environmental concerns.

4. Higher Costs for Consumers: When industries successfully capture regulators, they can use their influence to shape rules and regulations that favor their own interests at the expense of consumers. This can result in higher prices for goods and services without providing any additional benefits.

5. Negative Impact on Competition: Regulatory capture can create barriers to entry for new competitors by erecting complex regulatory frameworks that benefit incumbent players who have already established strong relationships with regulators through lobbying efforts.

6. Reduced Innovation: Industries that have successfully captured regulators may resist changes that could disrupt their existing business models or introduce new technologies or practices from emerging competitors. This resistance hampers innovation and stifles progress in vital areas such as healthcare, energy, and technology.

7. Undermined Democracy: By allowing powerful special interests undue influence over regulation, regulatory capture weakens democratic principles by giving disproportionate power to narrow groups at the expense of broader societal welfare.

The consequences of regulatory capture should not be underestimated as they have far-reaching implications for society as a whole – from eroding public trust to distorting policies and hindering competition and innovation. It is imperative for governments and regulators to remain vigilant and take steps.

How to Prevent Regulatory Capture

Preventing regulatory capture is crucial for maintaining a fair and transparent regulatory environment. While completely eliminating the risk may be challenging, there are several strategies that can help mitigate its occurrence.

1. Strong Transparency Measures: Promoting transparency in decision-making processes is essential. This includes requiring regulators to disclose their interactions with industry stakeholders, making meeting minutes and documents publicly available, and ensuring that conflicts of interest are properly disclosed.

2. Robust Oversight Mechanisms: Establishing independent oversight bodies can help monitor regulatory agencies and ensure they act in the public interest. These bodies should have sufficient resources and authority to investigate potential instances of capture and hold regulators accountable for any wrongdoing.

3. Rotating Staff and Revolving Door Restrictions: Regularly rotating staff within regulatory agencies can reduce the likelihood of undue influence by specific industries or individuals. Additionally, implementing cooling-off periods or restrictions on regulators transitioning directly into private sector positions related to their former responsibilities helps prevent conflicts of interest.

4. Public Participation: Actively involving the public in the rulemaking process allows diverse perspectives to be considered, reducing the chances of capture by narrow interests. Public consultations, open hearings, and soliciting feedback from affected parties enable greater accountability and legitimacy in regulatory decision-making.

5. Continuous Education: Ensuring that regulators possess a deep understanding of industry practices while also being aware of potential risks is vital for effective regulation. Providing ongoing training programs on ethics, conflict resolution, policy analysis, economics, etc., equips regulators with the necessary tools to navigate complex policymaking environments more effectively.

By implementing these preventive measures collectively or individually as appropriate for each jurisdiction's context, the risk of regulatory capture can be significantly reduced.

Conclusion

Regulatory capture is a serious issue that can have far-reaching consequences for society. It occurs when regulatory agencies, which are supposed to protect the public interest, become influenced or controlled by the industries they are meant to oversee. This phenomenon undermines the effectiveness of regulation and creates an environment where special interests hold more power than the general welfare.

The causes of regulatory capture are multifaceted and often intertwined with political and economic factors. The revolving door between industry and government, inadequate funding and resources for regulatory agencies, and asymmetrical information all contribute to this problem. Additionally, regulatory agencies may develop cozy relationships with regulated entities over time, leading to a loss of independence.

The consequences of regulatory capture can be detrimental. When regulations favor certain industries or companies at the expense of others or fail to adequately address risks, it can lead to market distortions, reduced competition, increased prices for consumers, compromised safety standards, environmental damage, and erosion of public trust in government institutions.

Preventing regulatory capture requires a multifaceted approach. Strengthening ethical standards for regulators through conflict-of-interest rules and transparency measures is crucial. Ensuring adequate funding and staffing levels for regulatory agencies is also vital so that they can fulfill their mandates effectively. Encouraging public participation in rule-making processes through open consultations can help prevent undue influence from powerful interests.

It is important for policymakers to acknowledge the existence of regulatory capture as a systemic problem that needs attention rather than dismissing it as isolated incidents. Regular evaluations should be conducted to identify signs of potential capture within agencies so that corrective actions can be taken promptly.

In conclusion (without using those exact words), understanding what drives regulatory capture empowers us to take steps towards preventing it from undermining effective regulation intended for promoting social good. By addressing its causes head-on while implementing comprehensive strategies aimed at enhancing transparency, accountability.

Creating a Favorable Investment Climate through Stable Monetary Policies

Creating a Favorable Investment Climate through Stable Monetary Policies

Welcome to our blog post on creating a favorable investment climate through stable monetary policies! In today's ever-changing economic landscape, it is crucial for countries to establish and maintain stability in their monetary policies. But what exactly does that mean? And why is it so important?

In this article, we will explore the concept of stable monetary policies, their significance in fostering economic growth, and how they contribute to maintaining a healthy investment environment. So grab your coffee and get ready to dive into the world of finance as we unravel the secrets behind successful monetary policy implementation!

What is a Stable Monetary Policy?

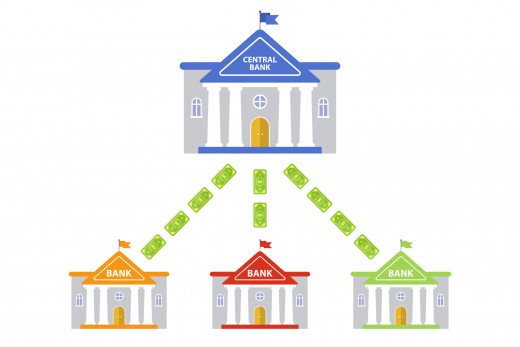

A stable monetary policy is a crucial aspect of any economy. It refers to the actions taken by a central bank or monetary authority to regulate and control the money supply, interest rates, and inflation in order to promote economic stability.

One key element of a stable monetary policy is maintaining price stability. This means ensuring that inflation remains low and predictable over time. By achieving price stability, it helps businesses and individuals make informed decisions about their spending, investments, and savings.

Another important aspect of a stable monetary policy is promoting sustainable economic growth. When there is stability in the economy, businesses are more likely to invest capital for expansion, which leads to job creation and increased consumer spending.

Additionally, a stable monetary policy helps maintain financial market stability. It reduces uncertainty among investors and encourages them to participate in various financial activities such as lending or borrowing funds.

To achieve these objectives, central banks use various tools such as open market operations (buying or selling government securities), adjusting reserve requirements for banks, or manipulating short-term interest rates.

The Importance of Stable Monetary Policies

A stable monetary policy plays a crucial role in fostering a favorable investment climate and driving economic growth. By maintaining price stability and promoting financial stability, it provides businesses and investors with the confidence they need to make long-term investment decisions.

Price stability is one of the key objectives of monetary policy. When prices are relatively stable, businesses can plan ahead without worrying about sudden spikes in costs or unpredictable inflation eroding their profits. This predictability encourages them to invest in new projects, expand operations, and create jobs.

Moreover, stable monetary policies help promote financial stability by reducing uncertainty in the financial markets. When interest rates are kept at reasonable levels over an extended period, it allows borrowers to plan their investments more effectively while also providing savers with a fair return on their investments.

In addition to promoting stability, a well-executed monetary policy can also address economic imbalances such as high unemployment or low inflation. Through its various tools like open market operations or adjusting interest rates, central banks can influence borrowing costs and credit availability to stimulate economic activity during downturns or rein in excessive inflationary pressures.

Central banks play a vital role in implementing these policies through independent decision-making processes based on data analysis and expert judgment. By setting clear objectives for price stability and employing appropriate tools, they ensure that monetary policies remain effective even during times of economic uncertainty.

To summarize briefly (without concluding), stable monetary policies are essential for creating an environment conducive to investment by providing businesses with certainty regarding prices and enabling them to plan future endeavors accordingly. Additionally, they promote financial stability by offering predictable returns on investments while addressing any underlying imbalances within the economy through targeted interventions when necessary.

Monetary Policy and Economic Growth

Monetary policy plays a crucial role in influencing economic growth. By managing the supply and cost of money, central banks can stimulate or restrict economic activity to maintain stability. When it comes to promoting economic growth, monetary policy focuses on factors such as interest rates, credit availability, and exchange rate management.

One way monetary policy supports economic growth is through interest rates. Lowering interest rates encourages borrowing and investment by making it cheaper for businesses and individuals to access credit. This stimulates spending and expands economic activity across various sectors.

Additionally, monetary policies that promote price stability help create a favorable environment for economic growth. Inflation erodes the purchasing power of consumers, reducing their ability to spend on goods and services. Through its control over inflation levels, central banks can ensure stable prices that support sustainable economic expansion.

Moreover, maintaining financial stability is another objective of monetary policy that contributes to long-term economic growth. Sound financial systems are essential for efficient allocation of resources and smooth functioning of markets. By implementing policies that regulate banks' activities and prevent excessive risk-taking, central banks foster confidence among investors which bolsters investment opportunities.

When implemented effectively with coherent objectives in mind, stable monetary policies can provide the necessary conditions for sustained economic growth by managing interest rates, controlling inflation levels,and ensuring financial stability.

The Relationship Between Inflation and Interest Rates

The relationship between inflation and interest rates is a crucial aspect of monetary policy. When inflation rises, central banks tend to increase interest rates as a means to curb excessive spending and keep prices stable. On the other hand, when inflation is low, central banks may lower interest rates to stimulate borrowing and investment.

Higher interest rates make borrowing more expensive for businesses and individuals. This reduces consumer spending and slows down economic growth. It also increases the cost of financing for businesses, which can discourage investments.

Conversely, lower interest rates encourage borrowing by making it cheaper. This stimulates consumer spending and boosts business investment in new projects or expansions. These measures aim to promote economic growth while keeping inflation at bay.

As such, central banks play a critical role in maintaining price stability through their control over interest rates. By carefully monitoring changes in inflation levels and adjusting policies accordingly, they strive to create an environment conducive to sustainable economic expansion.

There is an intricate relationship between inflation and interest rates that directly impacts both consumers' purchasing power and businesses' investment decisions. Central banks use this link as a tool to facilitate economic growth while guarding against the dangers of runaway inflation.

What are the Objectives of Monetary Policy?

Monetary policy plays a crucial role in shaping the economy, and its objectives are of utmost importance. The primary objective is to maintain price stability, which means keeping inflation low and stable. This ensures that the value of money remains relatively constant over time.

Another key objective is promoting sustainable economic growth. By influencing interest rates and credit availability, monetary policy can stimulate investment and consumption, leading to increased economic activity.

Additionally, monetary policy aims to stabilize financial markets by ensuring their smooth functioning. Central banks monitor market liquidity and respond accordingly to prevent disruptions that could negatively impact the overall economy.

Moreover, maintaining full employment is an essential goal of monetary policy. By managing interest rates and controlling inflation expectations, central banks can support job creation and reduce unemployment rates.

Furthermore, exchange rate stability is also an objective of monetary policy for countries with flexible exchange rate regimes. Stable exchange rates promote international trade by providing certainty for businesses engaged in global commerce.

The objectives of monetary policy are interconnected as they seek to create favorable conditions for sustained economic growth while maintaining price stability and addressing various macroeconomic challenges. Through effective implementation of these objectives, central banks contribute significantly towards creating a conducive investment climate that benefits both individuals and businesses alike.

How does the Fed Conduct Monetary Policy?

The Federal Reserve, commonly known as the Fed, plays a crucial role in conducting monetary policy in the United States. So how does the Fed navigate this complex task?

One of the key tools used by the Fed is open market operations. This involves buying and selling government securities to influence the level of reserves in banks. By increasing or decreasing these reserves, they can effectively impact interest rates and stimulate or cool down economic activity.

Another method employed by the Fed is adjusting reserve requirements for banks. By changing the amount of money that banks are required to keep on hand, they can control how much lending takes place within an economy. Lowering reserve requirements encourages more lending and boosts economic growth.

Furthermore, the Fed also utilizes its ability to set short-term interest rates through Negotiating Free Trade Agreements: Opportunities and Challenges is known as the federal funds rate. This rate serves as a benchmark for other interest rates throughout financial markets and has a direct effect on borrowing costs for businesses and consumers alike.

Additionally, forward guidance is another tool employed by the Fed to communicate their intentions regarding future monetary policy decisions. By providing clear guidance on their objectives and expected actions, they aim to shape market expectations and influence long-term interest rates.

While not directly related to conducting monetary policy itself but still important nonetheless is transparency. The Fed regularly communicates its decisions and rationale behind them through public statements and press conferences. This helps maintain trust in their actions among market participants.

Through various mechanisms such as open market operations, reserve requirements adjustments, setting short-term interest rates like federal funds rate along with forward guidance communication strategies plus maintaining transparency; The Federal Reserve skillfully conducts monetary policy ensuring stability in our nation's economy without compromising growth potential!

Negotiating Free Trade Agreements: Opportunities and Challenges

Negotiating Free Trade Agreements: Opportunities and Challenges

Welcome to our blog post on the fascinating world of negotiating free trade agreements! Whether you're an economics enthusiast, a business owner looking for new opportunities, or simply curious about how countries establish economic partnerships, this article will provide you with valuable insights into the intricacies of free trade negotiations. From understanding what these agreements are all about to exploring their potential benefits and challenges, we'll delve deep into the subject. So fasten your seatbelts as we embark on a journey through the exciting realm of international trade diplomacy! Get ready to discover how nations navigate through complex negotiations in search of mutually beneficial outcomes. Let's dive right in!

What is a Free Trade Agreement?

A Free Trade Agreement, also known as an FTA, is a pact between two or more countries to facilitate the flow of goods and services across borders by reducing or eliminating trade barriers. These agreements are typically negotiated with the aim of promoting economic growth and increasing market access for participating nations.

In a free trade agreement, countries agree to lower tariffs and quotas on imports and exports, allowing businesses to compete on a level playing field. This helps to stimulate international trade by making it easier and cheaper for companies to sell their products in foreign markets.

One of the key benefits of free trade agreements is that they can lead to increased efficiency and specialization. By removing barriers, countries can focus on producing goods and services that they have a comparative advantage in, leading to greater productivity gains.

However, there are also potential downsides. Critics argue that free trade agreements can lead to job losses in certain industries as domestic producers struggle to compete with cheaper imports. Additionally, concerns have been raised about issues such as environmental standards and intellectual property rights being potentially undermined by these agreements.

Negotiating a free trade agreement involves complex discussions between participating nations. Governments must consider various factors such as protecting sensitive industries while still seeking opportunities for market access abroad. It requires striking a delicate balance between national interests and creating mutually beneficial outcomes for all parties involved.

Recent examples of successful negotiations include the United States-Mexico-Canada Agreement (USMCA) replacing NAFTA, which aims at modernizing rules governing North American commerce. The Comprehensive Economic Partnership Agreement (CEPA) signed between India and South Korea is another notable example.

Challenges abound when negotiating free trade agreements due to differences in political systems, cultural nuances, economic priorities, and regulatory frameworks among participating countries. Disputes over contentious issues like agriculture subsidies or intellectual property rights can stall negotiations indefinitely if not adequately addressed.

The Pros and Cons of Free Trade Agreements

Free Trade Agreements (FTAs) have both advantages and disadvantages for participating countries. One of the key benefits is increased market access. By eliminating or reducing tariffs and trade barriers, FTAs open up new opportunities for businesses to expand into foreign markets. This can lead to higher export levels and increased economic growth.

Another advantage of FTAs is enhanced competitiveness. When countries engage in free trade, they are forced to become more efficient and productive in order to compete with international rivals. This can drive innovation, improve product quality, and lower prices for consumers.

Furthermore, FTAs promote specialization by allowing countries to focus on producing goods or services that they excel at while importing others that may be produced more efficiently elsewhere. This increases overall efficiency and maximizes resource utilization.

On the flip side, one of the main concerns about FTAs is potential job displacement. As industries face competition from abroad, some jobs may be lost domestically due to outsourcing or lack of competitiveness. However, proponents argue that this short-term pain can lead to long-term gains as resources shift towards more efficient sectors.

There are also concerns about unequal distribution of benefits within a country. While certain industries may thrive under an FTA, others might struggle to remain competitive or adapt quickly enough. It's important for governments to provide support and assistance during periods of adjustment.

Critics argue that FTAs could undermine domestic regulations on issues such as labor rights, environmental protection, and public health standards if not properly addressed in the negotiation process.

Overall, the pros and cons of Free Trade Agreements must be carefully weighed before entering into negotiations. Each agreement comes with its own unique set of opportunities and challenges, so it's essential to consider all aspects when determining whether a particular FTA will benefit a nation's economy in the long run.

How to Negotiate a Free Trade Agreement

Negotiating a free trade agreement requires careful planning, strategy, and diplomacy. Here are some key steps to consider when approaching the negotiation process.

It is important to conduct thorough research on the potential partner country or countries. This includes understanding their economic landscape, market conditions, and any existing trade barriers. By gathering this information, you can identify areas of mutual benefit and potential obstacles that may arise during negotiations.

Next, define your objectives clearly. What do you hope to achieve through this agreement? Is it increased market access for your goods and services? Tariff reductions? Intellectual property protections? By having specific goals in mind, you can focus your efforts on negotiating favorable terms in these areas.

Effective communication is crucial throughout the negotiation process. Be prepared to clearly articulate your position and listen actively to the concerns of the other party. Finding common ground and addressing any differences constructively will help build trust and facilitate progress in the negotiations.

Flexibility is another essential trait when negotiating a free trade agreement. It's important not to be rigid in your approach but instead be open to compromise where necessary while still protecting your core interests. Negotiations often involve give-and-take from both parties involved.

Ensure transparency throughout the negotiation process by involving relevant stakeholders such as industry representatives or experts who can provide valuable insights into specific sectors affected by the agreement.

Negotiating a free trade agreement can be complex and challenging; however, with careful planning, effective communication skills, flexibility, and transparency processes can lead to mutually beneficial outcomes for all parties involved.

Recent Examples of Free Trade Agreements

In recent years, there have been several notable examples of free trade agreements that have shaped global economic dynamics. One such agreement is the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), which came into effect in 2018. It involves 11 countries, including Japan, Canada, Australia, and Singapore. By reducing tariffs and removing trade barriers, this agreement aims to promote economic integration among member nations.

Another significant example is the United States-Mexico-Canada Agreement (USMCA). This trilateral agreement replaced the North American Free Trade Agreement (NAFTA) and seeks to modernize trade relations between these three countries. It addresses issues related to labor rights, intellectual property protection, digital trade, and environmental standards.

The European Union has also been actively engaged in negotiating free trade agreements with various regions across the globe. For instance, the EU-South Korea Free Trade Agreement has expanded market access for both sides while facilitating a smoother flow of goods and services.

Additionally, several African nations are pursuing regional free trade agreements as part of efforts to boost intra-African trade. The African Continental Free Trade Area (AfCFTA), launched in 2021 after years of negotiations, aims to create a single market for goods and services across 54 African countries.

These recent examples highlight how free trade agreements continue to play a crucial role in shaping global commerce. While each agreement varies based on the specific needs and interests of participating nations, they all strive towards enhancing economic cooperation and fostering mutual growth opportunities.

Challenges in Negotiating Free Trade Agreements

Negotiating free trade agreements can be a complex and challenging process. One of the biggest challenges is reaching an agreement that satisfies all parties involved. Each country has its own interests and priorities, which can sometimes clash with those of other countries.

Another challenge is finding a balance between protecting domestic industries and opening up market access. Countries may want to protect their own industries from foreign competition, but at the same time, they also want to benefit from increased market access for their exports.

The negotiation process itself can be lengthy and arduous. It requires extensive research, analysis, and compromise on various issues such as tariffs, intellectual property rights, services trade, and regulatory standards. Negotiators must navigate through complex legal frameworks and conflicting national policies.

Additionally, there are often political considerations that come into play during negotiations. Domestic pressure groups may lobby against certain provisions or demand more favorable terms for specific industries or sectors. This adds another layer of complexity to the negotiation process.

Furthermore, negotiating free trade agreements involves dealing with different cultural norms and practices across countries. Language barriers, differences in business customs, and varying levels of economic development can all contribute to misunderstandings or disputes during negotiations.

In conclusion (not conclusive), negotiating free trade agreements is no easy task due to the multitude of challenges involved – from reconciling competing interests to navigating political pressures – it requires skillful diplomacy and perseverance from negotiators on all sides.

Leveraging Artificial Intelligence for Smart Regulation

Leveraging Artificial Intelligence for Smart Regulation

Artificial Intelligence (AI) has become a game-changer in various industries, revolutionizing the way we live and work. From virtual assistants like Siri to self-driving cars, AI has seamlessly integrated into our daily lives. But did you know that this powerful technology can also be harnessed for smart regulation? That's right!

In this blog post, we will explore how AI is transforming the regulatory landscape and why it's time to leverage its incredible potential. So fasten your seatbelts as we embark on an exciting journey into the world of AI-powered smart regulation!

What is Artificial Intelligence?

Artificial Intelligence, or AI for short, is a branch of computer science that focuses on creating intelligent machines capable of performing tasks that typically require human intelligence. It involves the development and implementation of algorithms and models that enable computers to learn from data, reason, make decisions, and even recognize patterns.

At its core, AI aims to replicate human cognitive abilities such as problem-solving, learning from experience, speech recognition, natural language processing, and decision-making. This technology has evolved significantly over the years thanks to advancements in computing power and access to vast amounts of data.

AI can be divided into two categories: Narrow AI and General AI. Narrow AI refers to systems designed for specific tasks like image recognition or voice assistants. On the other hand, General AI strives to create machines with human-like capabilities across multiple domains.

Machine Learning (ML) is a critical component of AI where algorithms are trained on data sets to identify patterns and make predictions or decisions without explicit programming instructions. Deep Learning is a subset of ML that uses artificial neural networks inspired by the structure and function of the human brain.

By harnessing these technologies together with various techniques like Natural Language Processing (NLP), Computer Vision (CV), Robotics Process Automation (RPA), and more; Artificial Intelligence has become an indispensable tool across industries ranging from healthcare and finance to transportation and entertainment.

As our understanding deepens about what artificial intelligence can accomplish, its potential applications continue expanding at an exponential rate. The possibilities seem limitless - whether it's automating routine tasks through chatbots or assisting doctors in diagnosing diseases accurately - we're only just scratching the surface when it comes to unleashing this extraordinary technology's full potential. So buckle up – because things are about to get even smarter!

How can Artificial Intelligence be used for Smart Regulation?

Artificial Intelligence (AI) has the potential to revolutionize the way we approach regulation. It can provide regulators with powerful tools to analyze vast amounts of data and make more informed decisions. AI can be used for smart regulation in various ways.

AI can help automate regulatory processes, reducing the need for manual intervention and improving efficiency. For example, AI algorithms can be trained to review large volumes of documents and identify any potential compliance issues or violations.

Furthermore, AI-powered predictive analytics can enable regulators to detect patterns and trends that may indicate future risks or non-compliance. By analyzing historical data, AI systems can proactively flag areas that require closer scrutiny, allowing regulators to take preventive action before problems escalate.

Another key application of AI in smart regulation is monitoring and enforcement. Through advanced machine learning techniques, AI systems can monitor market activities in real-time and identify suspicious behavior or illegal activities such as insider trading or market manipulation.

Moreover, natural language processing capabilities of AI technology enable regulators to better understand public sentiment by analyzing social media posts or online discussions related to specific industries or companies. This valuable information helps shape regulatory strategies and interventions based on public concerns.

Additionally, by leveraging machine learning algorithms, regulators can develop risk assessment models that are continuously updated based on new data inputs. These models allow for a more dynamic understanding of risks within regulated sectors and help prioritize resources accordingly.

Artificial Intelligence offers immense opportunities for smart regulation across various domains including automation of processes, predictive analytics for risk identification, real-time monitoring and enforcement capabilities as well as improved understanding of public sentiment through analysis of unstructured data sources like social media. Harnessing these capabilities effectively will undoubtedly lead to more efficient and effective regulatory outcomes while promoting innovation in industries subjected to regulations.

The Benefits of using Artificial Intelligence for Smart Regulation

Artificial Intelligence (AI) has revolutionized various industries, and the field of regulation is no exception. The use of AI for smart regulation brings numerous benefits that can enhance efficiency, accuracy, and effectiveness in regulatory processes.

One significant benefit of using AI for smart regulation is improved data analysis capabilities. With vast amounts of data to analyze, AI algorithms can quickly process and extract valuable insights from complex datasets. This enables regulators to make informed decisions based on real-time information, leading to more proactive and effective regulations.

Additionally, AI-powered systems can automate repetitive tasks, freeing up valuable time for regulators to focus on higher-value activities. By automating processes such as data collection, monitoring compliance, and risk assessment, regulators can streamline operations and allocate resources more efficiently.

Another advantage of leveraging AI in smart regulation is its ability to detect patterns or anomalies in large datasets that may be challenging for humans to identify manually. These advanced analytical capabilities enable early detection of potential risks or non-compliance issues, allowing regulators to take timely action before they escalate into larger problems.

Furthermore, AI technologies like natural language processing (NLP) can help improve regulatory transparency by enabling automated analysis of text-based documents such as laws, regulations, and policy guidelines. This ensures consistent interpretation across different jurisdictions while reducing ambiguity or inconsistencies that may arise due to human error.

In summary, the benefits of using AI for smart regulation are numerous. From enhanced data analysis capabilities to automation and improved regulatory transparency, AI offers tremendous potential for transforming the regulatory landscape. However, it's crucial to address the risks associated with relying solely on machine-driven decision-making without appropriate human oversight. By striking a balance between technological advancements and human judgment, we can unlock the full potential of artificial intelligence in driving smarter regulations.

The Risks of using Artificial Intelligence for Smart Regulation

Artificial Intelligence (AI) has undoubtedly revolutionized various industries, including regulation. While there are numerous benefits to leveraging AI for smart regulation, it is crucial to acknowledge and address the risks associated with its implementation.

One significant risk of using AI for smart regulation is the potential for algorithmic bias. AI systems are trained on vast amounts of data, which can inadvertently contain biases present in society. If these biases go unnoticed or unchecked, they can perpetuate discriminatory practices or outcomes within the regulatory process.

Another risk lies in the transparency and accountability of AI algorithms. Unlike traditional regulations that are developed by humans and subject to scrutiny and oversight, AI algorithms operate based on complex models that may be difficult to understand fully. This lack of transparency raises concerns about how decisions made by AI systems align with legal frameworks and ethical standards.

Additionally, reliance on AI for smart regulation requires ensuring robust cybersecurity measures. The more we rely on interconnected technologies powered by AI systems, the higher the vulnerability to cyber threats becomes. Malicious actors could exploit vulnerabilities in these systems to manipulate regulatory processes or gain unauthorized access to sensitive information.

Furthermore, integrating AI into smart regulation necessitates careful consideration of privacy concerns. As regulators collect and analyze massive volumes of data from various sources through machine learning algorithms, preserving individuals' privacy becomes paramount. Striking a balance between utilizing data-driven insights while protecting personal information poses a challenge that needs diligent attention.

There is an inherent concern regarding job displacement due to automation through artificial intelligence in regulatory agencies themselves. While introducing AI can streamline processes and increase efficiency, it may also lead to workforce reductions if not managed thoughtfully.

Addressing these risks requires proactive measures such as developing robust governance frameworks specific to regulating artificial intelligence applications effectively. These frameworks should encompass comprehensive audit mechanisms that ensure fairness, accountability, transparency while minimizing biases at every stage of development and deployment.

How to Implement Artificial Intelligence for Smart Regulation

Implementing Artificial Intelligence for smart regulation requires careful planning and strategic execution. Here are some key steps to consider:

1. Define the objectives: Start by clearly identifying the goals you want to achieve with AI in regulation. Whether it's improving efficiency, detecting fraud, or ensuring compliance, having a clear focus will guide your implementation strategy.

2. Gather quality data: AI systems heavily rely on data to make accurate predictions and decisions. Collect relevant and reliable datasets that reflect the specific regulatory challenges you aim to address. Ensure that the data is diverse, up-to-date, and properly labeled.

3. Choose the right algorithms: Different AI algorithms are suited for different tasks. Select algorithms that align with your regulatory needs, whether it's machine learning models for pattern recognition or natural language processing tools for analyzing textual information.

4. Train and test your models: Once you have chosen an appropriate algorithm, train it using your dataset to enable it to learn patterns and make informed predictions or classifications accurately. Test its performance rigorously before deploying it in real-world scenarios.

5. Establish transparency and accountability: It is crucial to ensure transparency when implementing AI in regulations so that both regulators and regulated entities understand how decisions are being made.

Explainability techniques such as rule-based explanations can help build trust among stakeholders.

6. Deploy incrementally: Rather than implementing AI across all regulatory processes at once, start small-scale pilot projects to assess its effectiveness before scaling up gradually.

This approach allows you to identify any potential issues early on while minimizing disruptions.

7. Monitor and evaluate continuously: Regularly monitor the performance of your implemented AI system against predefined metrics.

Evaluate its impact on regulatory outcomes periodically.

Make necessary adjustments based on feedback received from users or any emerging risks identified during monitoring process.

By following these steps carefully, organizations can successfully implement Artificial Intelligence solutions into their smart regulation practices while mitigating potential risks.

Implementing Policies to Promote Innovation and Entrepreneurship

Implementing Policies to Promote Innovation and Entrepreneurship

Welcome to our blog post on implementing policies to promote innovation and entrepreneurship! In today's rapidly evolving world, where technology is advancing at an unprecedented pace, fostering a culture of innovation and encouraging entrepreneurial endeavors has become more important than ever. Innovation drives economic growth, creates jobs, and improves the quality of life for individuals and communities. That's why governments around the globe are actively introducing policies aimed at supporting and nurturing innovation and entrepreneurship.

In this article, we will explore some of these policies, their impact on promoting innovation and entrepreneurship, as well as their overall success in driving positive change. So let's dive right in!

The Importance of Innovation and Entrepreneurship

Innovation and entrepreneurship are the driving forces behind progress and prosperity in any society. They fuel economic growth, create job opportunities, and spur technological advancements that shape our future.

Innovation is about finding new ways to solve problems, introducing groundbreaking ideas, and challenging the status quo. It pushes boundaries, disrupts industries, and opens up possibilities we never thought possible. Whether it's a revolutionary product design or a breakthrough scientific discovery, innovation propels us forward.

Entrepreneurship goes hand in hand with innovation by taking those innovative ideas and turning them into tangible businesses or ventures. Entrepreneurs are risk-takers who see opportunities where others may not; they have the drive to bring their visions to life.

Both innovation and entrepreneurship contribute significantly to enhancing competitiveness on a global scale. They foster resilience in times of uncertainty by encouraging adaptability and agility within business ecosystems.

Moreover, fostering an environment that supports these endeavors attracts talent from diverse fields while retaining local expertise. This leads to increased investment inflows as well as knowledge transfer between different sectors.

Embracing innovation and entrepreneurship lays the foundation for sustainable economic growth while addressing societal challenges through creative solutions. By recognizing their importance, governments can take proactive steps towards implementing policies that encourage this culture of innovation - policies we'll explore further in the next section!

Government Policies to Promote Innovation and Entrepreneurship

Governments around the world play a crucial role in fostering innovation and entrepreneurship. They have the power to shape policies that create an environment conducive to growth, creativity, and risk-taking. By implementing specific measures, governments can encourage individuals and businesses to embrace innovation and embark on entrepreneurial ventures.

One important policy is providing financial support through grants or loans specifically targeted at startups and small businesses. These funds can help cover initial costs such as research and development, hiring talent, or acquiring necessary equipment. Additionally, offering tax incentives for innovative companies allows them to reinvest their profits into new projects or expand their operations.

Another effective policy is investing in education and training programs focused on entrepreneurship. By equipping individuals with the skills needed to start their own businesses, governments empower citizens to take risks while providing them with valuable tools for success. Furthermore, creating partnerships between universities or vocational institutions and industry leaders can bridge the gap between academia and real-world business practices.

In order to foster collaboration between entrepreneurs, policymakers should establish incubators or innovation hubs where like-minded individuals can connect, share ideas, receive mentorship from experienced professionals, access resources such as co-working spaces or laboratories.

The Success of Government Policies in Promoting Innovation and Entrepreneurship

Government policies play a crucial role in fostering innovation and entrepreneurship within a country. These policies aim to create an enabling environment that encourages the growth of new ideas, startups, and businesses. By providing support and resources, governments can help individuals turn their innovative concepts into successful ventures.

One way in which government policies have been successful is through the establishment of incubators and accelerators. These programs provide mentorship, funding, and networking opportunities for aspiring entrepreneurs. They create an ecosystem where innovative ideas can flourish by offering guidance on business development strategies and connecting entrepreneurs with potential investors.

Additionally, governments have implemented tax incentives to encourage investment in research and development (R&D). By reducing the financial burden associated with R&D activities, these incentives motivate companies to invest more in innovation. This leads to advancements in technology, improved products or services, job creation, and overall economic growth.

Moreover, many governments have simplified bureaucratic processes involved in starting a business. By streamlining procedures like company registration or obtaining permits/licenses for operations, they reduce barriers to entry for entrepreneurs. This allows them to focus on developing their ideas without being hindered by excessive paperwork or delays.

Furthermore, some governments offer grants or subsidies specifically targeted at promoting innovation-driven sectors such as clean energy or biotechnology. By providing financial assistance to companies operating within these industries, governments stimulate technological advancements while addressing pressing societal issues like climate change or healthcare.

Conclusion

In today's fast-paced and competitive world, innovation and entrepreneurship play a crucial role in driving economic growth and societal progress. Governments around the globe recognize the importance of fostering an environment that encourages innovation and supports aspiring entrepreneurs.

Through various policies and initiatives, governments aim to create a conducive ecosystem for innovation and entrepreneurship. These policies include providing financial support, offering tax incentives, promoting research and development activities, streamlining regulatory processes, facilitating access to capital, and nurturing talent through education and training programs.

While the success of government policies in promoting innovation and entrepreneurship can vary from country to country, there is no denying their positive impact on economies worldwide. Many nations have witnessed remarkable growth in startup ecosystems, with innovative ideas turning into successful businesses that generate employment opportunities.

However, it is essential to continuously evaluate these policies' effectiveness by monitoring key metrics such as the number of startups launched, job creation rates within the entrepreneurial sector, investment inflows into innovative ventures. This evaluation will help policymakers identify areas where improvements are needed or new strategies need to be implemented.

To truly reap the benefits of innovation-driven economies in this rapidly evolving global landscape requires ongoing commitment from governments as well as collaboration between public institutions academia private industry venture capitalists entrepreneurs themselves.

Ultimately it is through sustained efforts by all stakeholders involved we can continue fostering a culture of creativity risk-taking technological advancement thus ensuring future generations inherit societies thrive on ingenuity entrepreneurial spirit.

Mastering the Key Components of Effective Management

Mastering the Key Components of Effective Management

As businesses and organizations continue to evolve in today's fast-paced world, the role of a manager has become more crucial than ever before. A skilled manager not only oversees daily operations but also plays a pivotal role in driving growth, fostering innovation, and ensuring employee satisfaction. But what exactly does it take to be an effective manager?

In this blog post, we will explore the key components that make up successful management and how you can master them to unleash your true leadership potential. So whether you're a seasoned professional or aspiring to climb the managerial ladder, get ready to dive into the world of effective management strategies and techniques that will set you apart from the rest!

The Role of a Manager

In any organization, the role of a manager is multi-faceted and requires a diverse set of skills. A manager serves as the bridge between upper management and employees, ensuring that organizational goals are effectively communicated and understood at all levels. They are responsible for overseeing day-to-day operations, making strategic decisions, and ensuring that resources are allocated efficiently.

One of the primary responsibilities of a manager is to provide guidance and support to their team members. This includes setting clear expectations, providing feedback and coaching, and fostering an environment where employees feel empowered to take ownership of their work. A skilled manager understands the strengths and weaknesses of each individual on their team and can leverage those talents to drive success.

Another crucial aspect of being a successful manager is effective communication. Managers must be able to articulate goals, objectives, and expectations clearly so that everyone is on the same page. Additionally, they should be active listeners who value input from their team members - after all, great ideas can come from anyone!

Flexibility is another key attribute that sets apart effective managers from others. In today's rapidly changing business landscape, adaptability is essential for navigating unforeseen challenges or shifts in priorities. A good manager remains open-minded while embracing new technologies or methodologies when necessary.

Lastly but certainly not least important: leaders lead by example! Managers must embody the qualities they want to see in their team members: integrity, accountability, professionalism - you name it! By demonstrating these traits consistently through actions rather than just words alone inspires trust among employees.

To sum it up briefly (without concluding): The role of a manager encompasses guiding teams towards achieving organizational goals through effective communication skills; understanding individual strengths within your team; being flexible amidst change; leading by example with integrity; thus creating an environment where both personal growth & professional development thrive.

The Skillset of an Effective Manager

The skillset of an effective manager is a crucial aspect of successful leadership. To excel in this role, managers must possess a diverse range of skills that enable them to navigate the challenges and complexities of their position.

First and foremost, effective communication skills are essential for managers. They must be able to clearly articulate goals, expectations, and provide feedback to their team members. Strong listening skills are equally important as they allow managers to understand the needs and concerns of their employees.

Problem-solving and decision-making abilities are also vital skills for managers. They need to analyze situations, identify potential solutions, weigh the pros and cons, and make informed decisions that benefit both the organization and its employees.

Furthermore, effective managers have strong organizational skills. They can prioritize tasks efficiently, manage time effectively, delegate responsibilities appropriately, and ensure projects are completed on schedule.

Leadership qualities such as empathy, integrity,and resilience play a significant role in being an effective manager. Empathy allows managers to connect with their team members on a personal level while understanding their perspectives. Integrity builds trust within the team by demonstrating honestyand ethical behavior. Resilience enables managers to adapt to unexpected challengesand setbacks without losing focus or motivation.

In addition, you should consider continuous learning as another important skill for an effective manager. Within dynamic work environments, it's crucial for manager to stay updated with new industry trends, strategies, and technologies. This ensures that they can lead from the forefront by incorporating innovative ideas into their management approach.

Overall, the skillset required for an effective manager encompasses various abilities including communication problem-solving, negotiation, time management, and leadership. These skills combined help create a positive work culture, foster employee growth, and drive organizational success.

The Different Management Styles

When it comes to effective management, there is no one-size-fits-all approach. Different managers adopt different management styles based on their personality, the needs of their team, and the organizational culture they operate in. Understanding these various management styles can help you become a more adaptable and successful leader.

One common style is autocratic management, where decisions are made solely by the manager without input from the team. This approach can be effective in situations requiring quick decision-making or when employees lack experience or knowledge.

On the other hand, democratic management involves involving team members in decision-making processes. This style promotes collaboration and empowers employees to contribute ideas and take ownership of their work.

Another popular style is laissez-faire management, which emphasizes minimal intervention from the manager. While this approach allows for creativity and freedom among team members, it also requires self-motivated individuals who can work independently.

In contrast to laissez-faire, transformational leadership focuses on inspiring and motivating employees to achieve their full potential. These leaders nurture strong relationships with their teams through mentorship and support.

There's situational leadership - an adaptive style that tailors approaches according to each situation or employee's needs. This flexible method ensures that managers adjust their expectations and guidance based on individual circumstances.

Understanding these different management styles enables you to assess your own strengths as a leader while recognizing areas for growth. By adopting a versatile approach that fits specific situations or teams' requirements best, you'll enhance your effectiveness as a manager overall.

Creating an Effective Management Plan

Creating an effective management plan is crucial for any organization to achieve its goals and maintain smooth operations. This plan serves as a roadmap that outlines the strategies, objectives, and actions required to effectively manage resources and drive success.

It is important to clearly define the goals and objectives of the organization. These should be specific, measurable, attainable, relevant, and time-bound (SMART). By setting clear targets, managers can align their teams' efforts towards achieving these goals.

Next, it's essential to identify and allocate resources appropriately. This includes human resources, financial budgets, technology infrastructure, and other necessary tools or equipment. Adequate resource allocation ensures that tasks are completed efficiently without unnecessary delays or bottlenecks.

Communication plays a vital role in effective management planning. Managers must establish open lines of communication with their team members to foster transparency and collaboration. Regular meetings should be scheduled to discuss progress updates, address concerns or challenges faced by employees while providing guidance or support when needed.

Furthermore, establishing key performance indicators (KPIs) helps track progress towards organizational goals on an ongoing basis. By regularly reviewing KPIs and adjusting strategies accordingly, managers can ensure they stay on track

Lastly, an effective management plan requires continuous evaluation and improvement. Managers need to assess whether the current strategies are yielding desired results or if adjustments need to be made. This could involve seeking feedback from employees, conducting performance reviews, making necessary changes based on market trends, or adapting processes as needed.

In summary, creating an effective management plan involves setting clear objectives, allocating resources appropriately, communicating effectively with team members, tracking progress through KPIs, and continuously evaluating strategies for improvement. By implementing these key components into their management plans, organizations can enhance productivity, boost, employee morale, and ultimately achieve long-term success.

Being an Effective Leader

Being an effective leader is not just about giving orders and expecting them to be followed. It's about setting a strong example, inspiring your team, and guiding them towards success. As a leader, it's important to have excellent communication skills, both in listening and speaking. By actively listening to your team members' ideas and concerns, you show that you value their input.

Another key aspect of being an effective leader is the ability to make tough decisions when necessary. This means weighing the pros and cons, considering different perspectives, and ultimately choosing the best course of action for the team as a whole.

Furthermore, successful leaders also possess strong emotional intelligence. They are able to understand and manage their own emotions while empathizing with others'. This allows them to build trust within their teams and create a positive work environment.

In addition to these qualities, effective leaders are also adaptable. They can navigate through change with ease and help guide their teams through any challenges that arise.

Good leaders lead by example. They embody the values they expect from their team members and hold themselves accountable for their actions.

Overall-being an effective leader takes time, effort, self-reflection,and continuous learning. It's about building relationships, supporting growth, and creating a collaborative culture where everyone feels valued.

The role of leadership goes beyond mere authority;it requires empathy, resilience, and dedication. Bit by honing these skills, you can become an exceptional leader who inspires others, to achieve greatness together.

Conclusion

Mastering the key components of effective management is essential for any aspiring leader. By understanding the role of a manager and acquiring the necessary skillset, individuals can excel in their leadership positions. It is vital to recognize that there are different management styles, each with its own strengths and weaknesses.

Creating an effective management plan allows managers to set clear goals, establish processes, and allocate resources efficiently. This helps streamline operations and ensures that all team members are aligned towards a common objective.

However, being an effective leader goes beyond just managing tasks and processes. It requires fostering open communication, building strong relationships with team members, providing support and guidance when needed, and empowering employees to reach their full potential.